Finch & Beak is now SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

We invite you to check out the SLR website, so you can see the full potential of what we offer, from sustainability strategies to implementation covering Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, Responsible Sourcing and more.

Publ. date 18 May 2022

Publ. date 18 May 2022Chemical distribution companies are often viewed as the companies responsible for the transport and storage of bulk and packaged chemicals, however these businesses’ typical activities include logistics such as packaging and (re-)labeling, as well as assisting clients in technical formulation, and R&D related activities. In 2020 the global Chemical Distribution market was valued at roughly EUR 230 billion, with an expected annual growth rate (CAGR) of 5.4% from 2020 to 2028.

Finch & Beak conducted a market research study, based on publicly available information, to identify the ESG maturity of European chemical distribution companies. A total of 38 companies, with a revenue of EUR >200 million were included in the research scope. Together, the 38 companies represent a market revenue of approximately EUR 54 billion.

To identify the ESG maturity, the 38 businesses were assessed using a Portfolio Sustainability Assessment, developed by the World Business Council for Sustainable Development. This assessment is twofold and looks at the operational vulnerability (the risks and opportunities of the environmental footprint and social handprint of the assessed company based on quantitative reported data), and the market alignment (showcasing the preparedness of companies on market related trends and developments).

Overall, the results show that 26% of the companies are leading the sector, referred to as Transformers. Those companies clearly set the pace and differentiate themselves from other companies in the sector by having a clear direction in place, which is reflected in the sustainability- and ESG programs. This group is followed by the Movers (26% of research scope), which are companies that have started focusing on ESG but are not mature yet. Clear targets, KPI’s and actions on sustainability are frequently missing. The last group is categorized as Traditionalists which comprises about half of the companies (48%) in the research scope. Those organizations are still to start their ESG journey as they lack ESG reporting and are less prepared to respond to risks related to sustainability and might miss out on new business opportunities that the current market trends are presenting.

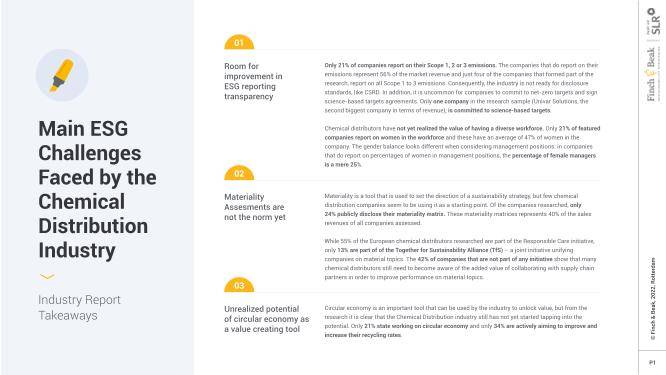

When it comes to setting direction for sustainability, only 24% of companies have conducted a materiality assessment. However, not all these companies report a forward-looking materiality matrix, in line with GRI guidelines and the upcoming CSRD requirements.

When looking at the disclosure of scope 1-3 emissions, it is further substantiated that chemical distributors lack transparent reporting. To date only 21% of the companies report on their scope 1, 2, or 3 emissions, representing 56% of market revenue. At current, Univar Solutions is the only organization that has committed to Science Based Targets. To move forward, joining the Race to Zero, it is of utmost important that chemical distributors, in collaboration with chemical manufacturers and clients, start collecting emission related data and follow through in their climate strategies and roadmaps.

On the social side, chemical distributors have not yet realized the value of having a diverse workforce. Only 21% of featured companies report on women in the workforce and these have an average of 47% of women in the company. The gender balance looks different when considering management positions: in companies that do report on percentages of women in management positions, the percentage of female managers is a mere 25%.

One of the ways to reach net zero ambitions, is by applying the principles of circular economy. At current only 31% of companies publicly disclose their recycling rates and only 1/5 of the companies mention to develop initiatives or programs related to circular economy, whereas the other companies are not publicly transparent on this matter. This showcases that the value is not captured yet and that the sector has a lot to gain especially since chemical distributors are heavily involved in R&D related activities, where integration of sustainability through the circular economy cannot be overlooked nowadays.

Looking at the potential for partnering on an industry level, 55% of the European chemical distributors are part of the Responsible Care initiative, while this is 13% of the Together for Sustainability Alliance. The results of the latter could partially be explained by the fact that most of the companies are family-owned businesses and are therefore not (yet) eligible to fall under stricter reporting requirements such as the European Corporate Sustainability Reporting Directive (entering into force in 2024).

One way for moving ahead is to increase ESG reporting maturity through participation in various ESG Benchmarks. A more common assessment today is the supplier assessment of EcoVadis, as chemical distribution companies are oftentimes asked by their clients to participate in this assessment, as currently 53% of companies have an EcoVadis ESG rating in place. Azelis is currently best in class, having received the Platinum Score recognition in 2021.

A second possible way forward for chemical distribution companies, as well as companies in the wider chemical value chain, is a portfolio sustainability assessment. This assessment looks at the sustainability maturity level on a product or product market combination level and shows insights on how well these perform on selected sustainability criteria. In the article written by Bettina Büchel, Professor of Strategy and Organization at IMD, (included in the report), a few best practices of Solvay and Evonik are highlighted to demonstrate how companies with a global operating scope are capturing the value of sustainability. As a result, they aim to optimize their operational procedures and processes, as well as following through on targets, and influencing supply chain partners to lower emissions.

Learn more about the research outcomes, how chemical distribution companies’ performance compares, gain insights from industry leaders, and find out how Finch & Beak can help your company to activate its ESG performance by downloading the full report.

Photo by Nenad Stokjovic on Flickr

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.