Finch & Beak is now SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

We invite you to check out the SLR website, so you can see the full potential of what we offer, from sustainability strategies to implementation covering Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, Responsible Sourcing and more.

Publ. date 10 Mar 2023

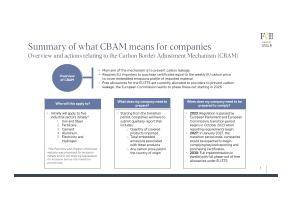

Publ. date 10 Mar 2023As a part of the European Union’s Fit for 55 initiative, the European Commission has introduced the concept of a Carbon Border Adjustment Mechanism (CBAM), with the aim of eliminating carbon leakage. This is to prevent that organizations could skirt carbon pricing mechanisms by importing goods from regions where these types of carbon pricing mechanisms are not yet in place.

Effectively, when organizations take this approach to importing, producers in the EU are facing unfair competition. This is because European producers, by participating in the European Union’s Emissions Trading Scheme (ETS), will have to pass through these carbon prices to the consumer, whereas other producers outside the bloc do not have to do so. The CBAM will, effectively, seek to eliminate this imbalance through requiring importers to pay a levy equivalent to a two-week average price of the EU ETS at the time of import.

Entry into force is anticipated for 2023, when only reporting requirements will be implemented. Companies will then have until 2026 before they are required to pay the additional fees. With this, organizations will be forced to reimagine and reevaluate their supply chains as former pricing advantages may diminish providing a strong business case for activating to decarbonize supply chains.

In the age of international supply chains where companies are often sourcing from partners worldwide, this regulation will have vast impacts on the way corporates think about their supply chains. In particular, in taking a closer look at Scope 3 emissions and reevaluating if imported goods will start to equalize in terms of pricing. This will have a particularly large impact on the five industrial sectors that were selected for the initial rollout of the mechanism. These industries are:

For the five selected industries, that were prioritized due to their potential for elevated carbon leakage, there will be two elements the companies will have to comply with. The first, during a transition period, organizations for whom the regulation applies will be responsible for producing a quarterly report that includes information on the quantity of covered products imported, total embedded emissions associated with these products, and any carbon price paid in the country of origin. The second element, will come only in 2026, when importers will be charged with purchasing emissions certificates equivalent to what would have been charged on the EU Emissions Trading System (EU ETS).

While these are the industries that will be the first targets of the regulation, the CBAM could also expand to include other industries after it enters into force. This would likely be with a focus on industries with high embedded carbon such as refined petroleum products, iron and ferrous ores, and more. The European Parliament had also initially proposed that the initial scope of the regulation be expanded to include organic chemicals and polymers, so this is likely one category that it is sure to assess whether to include in the scope before the transition period ends.

The downloadable summary at the top of the article provides an overview on CBAM and suggest how companies can start preparing for the new regulation.

For companies who have already created a strong approach to the management of supply chain issues, it is likely that the organization will have a strong foundation to comply with the new regulations. Having visibility on its suppliers will be crucial for a company to understand the relevant carbon pricing legislation that is in place, and to be able to quantify the embedded emissions of a product that the organization is sourcing from abroad.

Many companies have worked to incorporate technology to gain better visibility in their supply chains, including the chemical industry. This, given the industries' possible inclusion in the scope of the CBAM will give the industry an important leg up.

However, even if the industry has made some initial progress, the chemical industry has a significant amount of work remaining to decarbonize its value chain. The various efforts that the industry is making and an exploration on roadblocks the industry faces can be further explored inFinch & Beak’s report on trends in the chemical distribution industry. A key takeaway from this report is that decarbonization efforts are tricky for chemical distribution companies, as there are few chemical products with net-zero emissions meaning that companies can only focus on the offset of product emissions. This means a big first step for companies is to start calculating emissions.

| For example, plastics, chemicals and refining company LyondellBasell had previous set emissions reductions targets for Scope 1 and Scope 2 emissions, but was only able to announce it was expanding its commitment to include Scope 3 emissions at the close of 2022. The company, in conducting detailed calculations on its emissions in the upstream and downstream value chain realized that global sourced electricity generation drives a significant amount of emissions (relevant for CBAM). At the same time, LyondellBasell acknowledges that it will have to engage with the value chain in an effort to drive change in further driving down Scope 3 emissions. |

While technology can be a powerful tool in helping to understand the path of products, utilizing impact measurement & valuation can also provide strong insights as to where a company has its impact. This is particularly true for being able to understand the production of raw materials upstream and have visibility on what percentage of the impacts of the products come from.

While this will help a company to comply with the CBAM regulations, it can also facilitate a company taking action on decarbonizing its value chain. As companies face more and more scrutiny for the emissions profiles of their products, companies can take the regulatory mandate as an opportunity to expand their emissions and reduce overall value chain emissions beyond just the raw material imports.

| As highlighted in the Finch & Beak report, the chemical distribution company IMCD has been carrying out analyses to assess a products environmental footprint and modeling different scenarios of the use-phase of customers. |

This approach of incorporating life-cycle analysis can help to drive customer savings and if a company wishes to further understand its impact on society it can expand its view to the approach of impact measurement & valuation. This can help to ensure that a company is not only prepared for CBAM regulations, but also more resilient against various social and environmental issues arising in the supply chain.

While companies do have a significant lead time to prepare for this regulation, see the below tips for how to ensure that the needle begins to move towards progress in decarbonizing your company’s supply chain.

Do you want to get a better grip on knowing and actively managing your company's main impacts along the value chain, and improve your ESG performance? Please contact us at hello@finchandbeak.com to learn more about how Finch & Beak can support you with TCFD alignment and Impact Measurement & Valuation.

Photo by Ahsanization on Unsplash

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.