Finch & Beak is now SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

We invite you to check out the SLR website, so you can see the full potential of what we offer, from sustainability strategies to implementation covering Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, Responsible Sourcing and more.

Publ. date 24 Apr 2023

Publ. date 24 Apr 2023The year 2022 marked a turning point. In the ESG rating arena, while the CDP Climate Change questionnaire introduced a biodiversity module for the first time, the CSA broadened the scope of industries to which the biodiversity module applies. From a corporate reporting perspective, by including a standard specifically aimed at biodiversity and ecosystems, the first set of draft ESRS, published last November and developed under the CSRD, also encourages companies to start developing an understanding of their impacts on biodiversity and taking actions to mitigate them as well as reporting such information provided that the topic meets a certain materiality threshold for the organization.

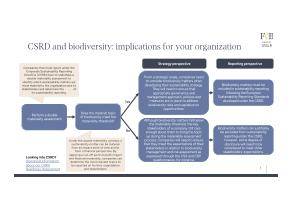

The expectations and requirements set by all three entities share some similarities by fostering companies to:

take inventory of biodiversity risks considering both dependency- and impact-related biodiversity risks by following internationally recognized methodologies/ frameworks (e.g., Task Force on Nature-related Financial Disclosures (TNFD), Natural Capital Protocol) and applying scenario analysis,

assess the exposure of their sites used for operational activities to critical biodiversity (e.g., number and size of sites in close proximity to critical biodiversity and their proximity to these areas),

publicly commit to addressing the identified biodiversity risks through policies and by setting a long-term net positive impact target on biodiversity, identifying priority areas (e.g., deforestation), supporting biodiversity-related initiatives with the endorsement of high-level management (board of directors, executive management)

translate these commitments into action through the implementation of measures and actions aiming at mitigating biodiversity impacts and progressing biodiversity-related commitments following a thorough mitigation hierarchy.

Besides this common ground, the CSRD takes a step further by expecting companies to ensure that their strategy and business model do no significant harm to nature by developing a robust transition plan that respects internationally recognized biodiversity targets. The standards also encourage companies to measure impact and monitor progress using biodiversity- and ecosystem change-related metrics and start quantifying potential financial effects of biodiversity and ecosystem-related risks and opportunities.

Download our guidance to determine how to address biodiversity matters from the CSRD standpoint at the top of the page. If you are looking for our CSRD-Readiness Assessment & Summer Package, you can find it in the download here.

Companies like Iberdrola, Mitsubishi Estate Group and Global Power Synergy Public Company Limited are demonstrating best practice examples when it comes to understanding and managing the topic of biodiversity within their organization.

Iberdrola has set an ambitious goal of having net positive impact on biodiversity by 2030 and developed an accompanying biodiversity plan that focuses on three logical pillars, namely, measuring impacts, taking actions based on the principle of conservation hierarchy and the results of measurement, transforming interactions with nature through cultural change.

As for Global Power Synergy Public Company Limited, the company has developed a comprehensive set of biodiversity commitments and guidelines to ensure proper management of biodiversity issues from risk assessment to action plan development.

Mitsubishi Estate Group demonstrates strong reporting practices about the outcomes of its biodiversity exposure assessments performed in collaboration with governments and/or in accordance with the Environmental Impact Assessment Act, depending on project scale, as well as about the actions taken to mitigate and reduce impacts as defined in internally developed guidelines.

Photo by Dario Brönnimann on Unsplash

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.