Thank you for visiting the Finch & Beak website. Finch & Beak is now part of SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

This is an exciting time for us, as our team now includes an array of new colleagues who offer advisory and technical skills that are complementary to our own including Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, and Responsible Sourcing.

We would like to take this opportunity to invite you to check out the SLR website, so you can see the full potential of what we are now able to offer.

Publ. date 15 Nov 2023

Publ. date 15 Nov 2023Read part 1 of the series "Leveraging CSRD Beyond Reporting" here |

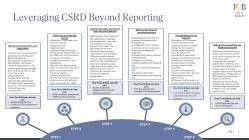

The accompanying download provides a comprehensive checklist of the recommended six steps to make sure organizations are on track on all fronts: complying with the CSRD while accelerating a company’s sustainability strategy and gaining a long-lasting competitive advantage.

This step focuses on aligning companies’ reporting framework with the recommendations of the CSRD, implementing missing policies and setting company-wide ESG targets.

Organizations are advised to pursue the following guidelines:

The recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) provide guidelines to assess and report the risks and opportunities organizations encounter in the face of climate change.

As a first step, companies are advised to conduct a TCFD-aligned climate risk assessment, including a scenario analysis to identify and assess climate-related impacts, risks and opportunities under different climate- related scenarios, including a 2°C or lower scenario.

Organizations should then define the impact of such risks and opportunities on the organization’s businesses, strategy, and financial planning and describe the resilience of the organization’s strategy. As a next step, organizations are recommended to implement a detailed transition plan for climate change mitigation and adaptation and allocate funding to support the implementation of this plan.

Furthermore, organizations should quantify the potential financial effects from physical and transition risks and opportunities. Lastly, companies are advised to sharpen their climate targets by setting science-based Net Zero targets and having them approved by the Science Based Targets initiative (SBTi).

The last step to leverage CSRD beyond reporting is to establish sustainability due diligence processes to assess social and environmental risks in the value chain and evaluate if the company’s approach to the management of impact is effective. Organizations are recommended to continuously engage with affected stakeholders to identify and evaluate the negative impacts on people and the environment.

Moreover, companies should ensure that steps are being taken to address and mitigate those negative impacts while tracking the effectiveness of these actions. Furthermore, it should be noted that the sustainability due diligence should be embedded within the organization’s governance, strategy and business model. As a final step, organizations should prepare the reporting structure FY2024 in line with CSRD requirements.

At Finch & Beak, we provide support for organizations as they prepare for CSRD, for example through materiality assessments, including a double materiality approach. If you are looking for support with your double materiality assessment or want to know more about how to link your risk management with sustainability, reach out to Johana Schlotter, Johana@finchandbeak.com or call +31 6 28 02 18 80.

Dynamic sustainability professional eager to help companies become a force for positive change. damien@finchandbeak.com

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.