Thank you for visiting the Finch & Beak website. Finch & Beak is now part of SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

This is an exciting time for us, as our team now includes an array of new colleagues who offer advisory and technical skills that are complementary to our own including Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, and Responsible Sourcing.

We would like to take this opportunity to invite you to check out the SLR website, so you can see the full potential of what we are now able to offer.

Publ. date 27 Oct 2021

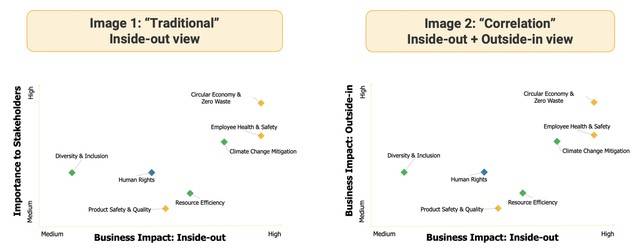

Publ. date 27 Oct 2021During Finch & Beak’s most recent ESG Acceleration Webinar, the topic of activation of the materiality matrix was one of the main features. During the webcast the audience was asked about the visualization of double materiality (referenced below). 11% of the audience voted in favor of a traditional display of material topics in which the stakeholder relevance is plotted against the assessment of business impact on society. In other words, what is the impact an organization has on the topics and with that indicating its contribution (both positive and negative) towards sustainable development.

29% of the audience indicated that a correlation matrix is a good way of displaying double materiality. The idea behind this correlation matrix is to show the outside-in impact of an organization (the financial impact materiality imperative) versus the inside-out impact of an organization (the societal impact materiality imperative). In this case, the stakeholder relevance is not included in the matrix. However, companies could opt for reporting on this in the narrative behind its most material issues. Alternatively, companies could opt for adding a third layer in their matrix by showing the size of the bubble as the stakeholder relevance input.

The most effective display of double materiality is still very much a matter of opinion. Almost 50% of the webinar audience indicated that the material issues should either be reported in a different matrix format or not in a matrix format at all, for instance in the form of a prioritization list. This list could be build based on the relevance the topics have towards your most important stakeholders, the impact it has on your organization (financial impact materiality), as well as the impact your organization has on the topics (societal impact materiality).

In their public reporting, companies could draw the line in terms of number of topics they want to touch upon. This approach also aligns with the latest updates of the GRI Standards, where it is no longer a requirement to represent your material topics in the format of a materiality matrix.

A company that is applying double materiality already is Merck Group, a German vibrant science and technology company. The concept of double materiality here is also pushed forward by the German Commercial Code in which this is included as a requisite.

In its public reporting, Merck lays out different sustainability categories with all having separate material issues underneath it. In this division, the company also ranks the topics from very high importance to medium importance and integrates a materiality threshold for inclusion. In addition, the company also displays its value chain and maps where the most material issues appear in what areas of the value chain.

From the examples above can be concluded that there is no best practice yet on how to visualize double materiality. What is currently known is that process should be thorough, complete, and documented. Moreover, a company is expected to measure both its impact on society as well as identifying what the impact is on the organization itself, whilst not omitting the perspective of its most important stakeholders.

If your organization is considering preparing for the upcoming CSRD and including double materiality in your next materiality assessment, get in touch with Johana Schlotter, at johana@finchandbeak.com or call +31 6 28 02 18 80 to hear about how Finch & Beak can support you in meeting your ambitions.

Image credit: Carlos ZGZ

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.