Thank you for visiting the Finch & Beak website. Finch & Beak is now part of SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

This is an exciting time for us, as our team now includes an array of new colleagues who offer advisory and technical skills that are complementary to our own including Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, and Responsible Sourcing.

We would like to take this opportunity to invite you to check out the SLR website, so you can see the full potential of what we are now able to offer.

Publ. date 3 Aug 2023

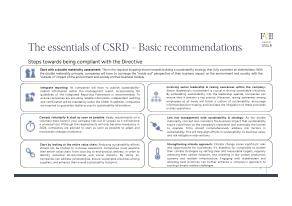

Publ. date 3 Aug 2023ESRS are the new cornerstone of a company’s sustainability reporting journey, serving as a roadmap to attract conscious investors and build trust among stakeholders. Data provided in traditional sustainability reports can lack depth or consistency, comprehensive metrics, and standardized guidelines, leading to questions about its reliability and resulting in potential skepticism among investors and stakeholders. The ESRS addresses these gaps, empowering companies to demonstrate their alignment with the European Green Deal Agenda.

Companies will undergo a phased implementation of ESRS, offering ample time for preparation, ensuring a smooth transition, and allowing companies to allocate sufficient time and resources to ensure compliance:

At the heart of the ESRS reporting process lies the critical element of a double materiality assessment. By adopting a "double materiality" approach, companies must report not only on their impact on people and the environment but also on how ESG issues create financial risks and opportunities. While the same sustainability topics included in the November 2022 EFRAG draft are confirmed as part of the double materiality assessment process, it is essential to note that companies should consider a broader spectrum of issues, beyond just the specified ESRS topics, to capture the full scope of their sustainability impact and challenges. As of the draft, the topics emphasized are:

| Category | ESRS Topics | |

| Environment | ESRS E1 Climate | |

| ESRS E2 Pollution | ||

| ESRS E3 Water and marine resources | ||

| ESRS E4 Biodiversity and ecosystems | ||

| ESRS E5 Resource use and circular economy | ||

| Social | ESRS S1 Own workforce | |

ESRS S2 Workers in the value chain |

||

| ESRS S3 Affected communities | ||

| ESRS S4 Consumers and end users | ||

| Governance | ESRS G1 Business conduct |

A robust double materiality assessment is then necessary to determine what is relevant or not among the different topics of the ESRS. It ensures that companies prioritize information that truly matters to their business and stakeholders, making their sustainability reporting more impactful and meaningful. This will avoid the costs associated with reporting information that may not be relevant. This is referred to as making more of the reporting requirements "subject to materiality" (i.e. it allows companies to omit information if it is not relevant in their particular circumstances), as opposed to being mandatory for all companies.

The robustness of the double materiality assessment remains consistent with mandatory disclosures absent except for ESRS 2 – General Disclosures. A significant shift, however, relates to climate change reporting under ESRS E1. If a company determines that climate change is not material to its operations, it is now required to elucidate the conclusions of its materiality assessment. This rationale should not just explain the current stance, but also project into the future. It involves analyzing potential scenarios—evaluating future contexts, challenges, and trends—in which climate change factors might become relevant or influence the company's strategy and operations in later evaluations.

Interestingly, this adaptation harks back to the initial drafts from November, where the mandatory nature of E1 was more pronounced. A conjecture arises from this: given the magnitude and reach of climate change, it is challenging to accept that companies of substantial size could dismiss it from their materiality. While some might venture this claim, the broader community awaits their rationale — or perhaps the potential absence of it — with keen interest.

Recognizing the significance of materiality assessment, the European Commission, in collaboration with the European Financial Reporting Advisory Group (EFRAG), will publish non-binding technical guidance on the application of ESRS. The forthcoming guidelines will provide companies with comprehensive support for conducting materiality assessments, with a particular focus on value chain analysis and the identification of financially material ESG factors.

In conclusion, ESRS presents a transformative opportunity for companies to take the lead in sustainability reporting and secure sustainable finance. Embracing these standards will empower companies to communicate their impact, inspire trust, and drive long-term success. As companies embark on their sustainability journey, it is vital to prioritize materiality assessments and diligently engage in the phased compliance process. Embrace ESRS not merely as a regulatory requirement but as a catalyst for sustainable growth, laying the foundation for a more resilient and prosperous future.

If your organization requires support on its double materiality journey, reach out to Johana Schlotter, at Johana@finchandbeak.com or call +31 6 28 02 18 80 to discuss how Finch & Beak can support you in meeting your ambitions, through our services:

Photo by Alex Mihis on Unsplash

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.