Thank you for visiting the Finch & Beak website. Finch & Beak is now part of SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

This is an exciting time for us, as our team now includes an array of new colleagues who offer advisory and technical skills that are complementary to our own including Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, and Responsible Sourcing.

We would like to take this opportunity to invite you to check out the SLR website, so you can see the full potential of what we are now able to offer.

Publ. date 13 Jul 2022

Publ. date 13 Jul 2022Materiality assessments are essential for organizations to build a strong base for their sustainability strategy, focus their efforts and communicate with their stakeholders on their non-financial performance. Moreover, the identification and disclosure of material sustainable development issues enhances organizations’ financial performance.

Given the importance of this exercise, stakeholder expectations (especially from regulation/reporting standards and investors) have become more strict on how this process should be conducted. Companies are now expected to prepare their materiality assessment in line with the principle of double materiality.

The concept of double materiality was introduced in the context of sustainability reporting given the need to get a full picture of an organization’s impacts, risks, and opportunities. Simply put, double materiality entails that organizations should consider a topic as material if it is relevant from either of the following perspectives:

New regulations and reporting standards such as the European Corporate Sustainability Reporting Directive (CSRD) require organizations to follow the double materiality principle. In late April 2022, the draft European sustainability reporting standards (ESRS), standards which the CSRD would adopt, were published for public consultation. These provide a first insight into what the reporting requirements in the CSRD will resemble, one important part of which is around double materiality.

Indeed, applying double materiality is essential to ensure that organizations consider the right topics in their materiality assessments, which is in turn, essential to properly build the sustainability strategy and communicate with stakeholders on the company’s non-financial performance.

For example, the topic of biodiversity may not have been identified as material yet by those organizations that only approached the materiality assessment from a financial-perspective, as this has been hard to measure so far. In contrast, organizations that had identified the topic to be material from an impact-perspective, i.e. meaning that biodiversity may be affected in the environment where the organization operates, have already started to address the topic (and are better prepared now that the topic is increasingly becoming material from a financial-perspective too).

An example of such a company is HeidelbergCement which identified its impact on biodiversity and responded by developing Group guidelines for the promotion of biodiversity at mineral extraction sites in 2010 already. This makes HeidelbergCement better equipped to address the topic of biodiversity, as it is becoming more material from a financial-perspective.

The increasing financial materiality of biodiversity can be observed with for instance the Taskforce on Nature-related Financial Disclosures framework being drafted to enable companies and financial institutions to integrate nature into decision making. More concretely, biodiversity’s financial materiality was confirmed this year with the introduction of biodiversity-related questions in investor-focused ratings such as CDP Climate Change and S&P Global’s Corporate Sustainability Assessment.

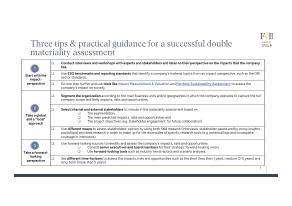

Determining how to approach and implement double materiality can be challenging. We suggest three things to consider as part of your organization’s double materiality approach and provide additional guidance in the downloadable checklist to assist you with the successful implementation thereof.

Topics which are material from an impact-perspective are likely to translate into financial effects in the short-, medium-, or long term. Therefore, starting with the impact-perspective can facilitate the identification of material topics. To understand the organization’s impacts on society, it is recommended to consult experts and stakeholders and conduct research on several ESG benchmarks and reporting standards that identify organizations’ material topics from an impact-perspective, such as the GRI sector standards.

Companies can also go one step further and use tools like Impact Measurement & Valuation and the Portfolio Sustainability Assessment to assess their impacts on society. This is for instance the approach that Novartis is taking: connecting materiality assessment to impact valuation to have a more quantitative approach and better inform its business strategies, management processes, and decision making.

The draft ESRS state that organizations should report on how their business model implementation and strategy take into account the interests of their stakeholders and of the impacts of the undertaking on sustainability matters. A double materiality assessment is an ideal opportunity to account for and report on these, as it requires active stakeholder engagement to properly assess the main impacts, risks, and opportunities that may arise from a financial as well as an impact perspective.

In order to assess the latter in a successful manner, it is recommended to take both a global and a “local” approach. This means considering the different geographies and/or business units that the company operates in, should the impacts, risks, and opportunities differ according to region or business unit.

Arkema followed this approach with its recent double-materiality assessment, consulting stakeholders across the different business lines and regions in which Arkema operates. This approach for a closer stakeholder dialogue is foundational to a successful materiality activation, for instance, to later engage in collaborations with industry partners to progress on specific topics.

Taking a forward-looking perspective is a key requirement in the draft ESRS. Considering emerging issues will allow companies to respond in time to these matters. This is increasingly important as can be seen with the new regulations being developed to better account for sustainability risks such as the updated Solvency II Directive for insurance companies: being required to take into account the potential long-term impact of their investment strategy and decisions on sustainability factors.

Consulting senior executives and board members, using forward-looking sources, and different time horizons, such as the short (less than 1 year), medium (2-5 years), and long-term (more than 5 years) is very helpful. AXA, for instance, uses different-time horizons to assess the material risks and issues that might impact its business in the short, medium, and long term each year with its internal and external stakeholders.

If you would like to know more about double materiality or require assistance with your materiality assessment and activation, get in touch with Johana Schlotter, at johana@finchandbeak.com or call +31 6 28 02 18 80 to discuss how Finch & Beak can support you.

Photo by Doun Rain AKA Tomas Gaspar on Unsplash

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.

.jpg?twic=v1/cover=720x405 "Double Materiality Built around the New Solvency II Directive")