Thank you for visiting the Finch & Beak website. Finch & Beak is now part of SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

This is an exciting time for us, as our team now includes an array of new colleagues who offer advisory and technical skills that are complementary to our own including Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, and Responsible Sourcing.

We would like to take this opportunity to invite you to check out the SLR website, so you can see the full potential of what we are now able to offer.

Publ. date 29 Jul 2022

Publ. date 29 Jul 2022According to a benchmarking study conducted by Finch & Beak aimed at understanding the ESG challenges facing the 25 largest Dow Jones Sustainability Index invited European insurance companies, 41% of companies cited climate change as one of their most material risks.

The

Through evaluating a sample of 10 of the top 25 European insurance companies selected for varying sustainability strategy maturity, it becomes clear that the application of TCFD principles is not uniform across the 4 key themes. When it comes to the governance dimension, there is a clear discrepancy in how the companies are describing the way in which management and Boards are involved in the evaluation of climate-related risks and opportunities. As part of their public reporting, 60% of the sampled insurance companies solely mention that the Board is informed on some climate issues or the overall risk profile.

Phoenix Group Holdings provides a strong case study of a best practice in this respect. Beyond assigning clear responsibility of oversight of the Group’s approach to climate risk and opportunity to the Board Sustainability Committee and oversight of the identification, assessment, management, and reporting of climate-related risks to the Board Risk Committee, Phoenix Group conducted training on regulatory requirements for TCFD, climate scenario analysis, and approaches to climate-related metrics and targets.

As part of the evaluation of the strategy dimension, 90% of the sampled companies in the Insurance industry provide in-depth explanations of the impact of climate-related risks and opportunities on the business, strategy, and financial planning in public reporting. The gap lies in identifying these risks and opportunities over various time frames (i.e., short, medium, and long term). In order to fully understand the risk, it is imperative that the companies are modeling out various climate scenarios (i.e. hothouse world vs. orderly transition) over several time frames (short-, mid-, and long-term) to truly understand the current risk and how it may evolve as applied to the company’s business strategy.

Companies are advised to clearly define timeframes and disclose the scenarios used to increase clarity as Allianz has done in listing out all aspects covered, scenarios used, and the scenario provider. The company has defined the short term as up to 3 years, the medium term as 3 to 10 years and the long-term as 10 plus years. The company then takes another step further and along 5-year increments from 2020 to 2040, it evaluates the asset and business impact under two transition scenarios as well as including risk enhancers and risk mitigators in the final analysis. This analysis is then integrated into the wider enterprise risk management framework which is considered a best practice. 70% of the sample followed suit in noting that the process for climate risk management is integrated within the larger enterprise risk management framework. Such performance on the risk management aspect is not surprising for an industry that has long been proficient in risk modeling as a part of both its business model and investing strategy.

The final dimension that is appraised is the metrics and targets, which is the dimension that seeks to identify how the organization discloses the metrics it uses to assess climate-related risks and opportunities, disclosing emissions and the related risks, and the targets used to manage climate-related risks and opportunities and performance against targets. The industry performs particularly poorly on disclosing its emissions and connecting them to the related risks. Only 40% of companies clearly disclose their own emissions and identify this as a climate risk. Often, the emissions are reported seemingly in isolation, like in the GRI Annex, and not acknowledged in how this lines up with the company strategy. Furthermore, the targets that are used to manage the risks and opportunities are often vague and not clearly linked to mitigating risks.

Generali serves as an inspiring best practice example in the way the company highlights various metrics and targets across physical and transition risks and opportunities. This includes highlighting the decarbonization of the general account investment portfolio to make it climate neutral by 2050 and highlighting that the company decreased its carbon intensity by 11.7 compared to 2020. The company also mentions an overachieved target related to opportunities for green and sustainable investments.

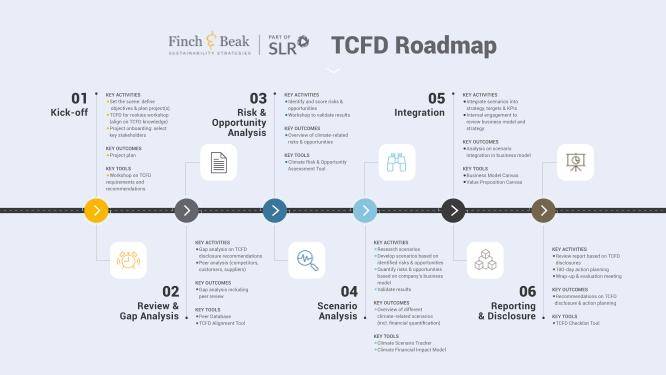

The downloadable Finch & Beak TCFD Roadmap available at the top of this article, is a useful tool to help your organization close these three or similar gaps and assist you in successfully implementing the recommendations.

If your organization is considering expanding your climate scenario analysis, or taking your climate-related financial disclosures to the next level then reach out to Johana Schlotter, at johana@finchandbeak.com or call +31 6 28 02 18 80 to discuss how Finch & Beak can support you.

Photo by Caleb Jones on Unsplash

Sustainability professional aiming to help companies implement practical strategies yielding positive ESG results. claire@finchandbeak.com

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.