Finch & Beak is now SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

We invite you to check out the SLR website, so you can see the full potential of what we offer, from sustainability strategies to implementation covering Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, Responsible Sourcing and more.

Publ. date 13 Oct 2021

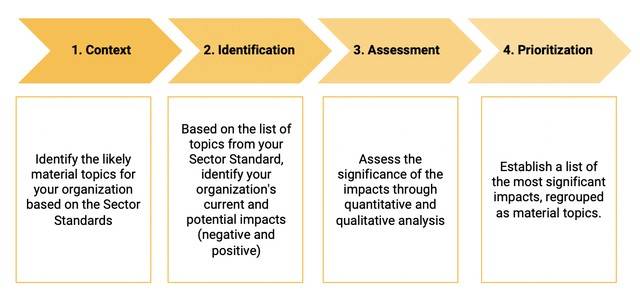

Publ. date 13 Oct 2021During its launch event, GRI announced the introduction of sector standards, aimed at helping companies to identify topics that are most likely to be material for each organization. The sector standards provide an additional grid to identify the relevant material issues. As such, identifying the likely material topics in your industry Standard is the recommended first step in the four-steps revised materiality process by GRI.

At this stage, GRI has only unveiled requirements for the Oil and Gas sector, which was identified as one of the most high-impact sectors based on the significance of the sector’s impact, its size and distribution around the world.

For the Oil and Gas Sector, 22 issues have been identified as likely material topics. Companies from the sector do not have to report on all material issues identified in their Sector Standard, but it is advised to consider them all when identifying the company’s impact (step 1 & 2: context and identification).

In the revised materiality assessment process, the starting point to identify material issues for your organization is the impact (actual and potential) that the company’s business activities can have on the economy, the environment, and people, including human right impacts. As such, GRI advocates for an assessment that considers all impacts (operational, reputational, or financial).

Impacts should not be deprioritized on the sole basis of not being considered financially material for the organization. Instead, impacts should be assessed based on the:

With the revised Universal Standards, the visual representation of the material topics should be a prioritized list of the issues and the selected threshold for reporting. A matrix representation is no longer required since the assessment no longer includes two independent criteria.

Through the updated GRI Standards, companies will have the choice of reporting (1) in accordance with the GRI Standards, or (2) with reference to the GRI Standards. The former refers to full compliance with all requirements, and the latter allows organizations to select their level of reporting through the GRI Standards guidelines. Organizations wishing to continue reporting according to the GRI Standards will need to move from the ‘Core’ / ‘Comprehensive’ approaches to these new guidelines by 2023.

A meaningful materiality assessment should capture the upcoming and emerging risks and impacts that will become key topics in the future. Keeping an eye on sector trends will strengthen views on the organization context (step 1) and make impact identification sharper (step 2). On risk assessment, the Global Risk Report published yearly by the World Economic Forum is a relevant tool.

GRI recommends organizations to engage with relevant stakeholders in the identification and assessment phases of their materiality assessment processes (steps 2 and 3). In this reviewed approach, stakeholder interest is no longer a separate variable of the materiality matrix (y-axis). It is rather an integrated dimension of the impacts’ assessment. Companies are advised to prioritize consultation of the stakeholders the most severely affected or potentially affected by the organization’s business activities.

A materiality assessment without activation is like a finch without a beak. To create value out of their materiality assessment, organizations are recommended to align their sustainability strategies on their assessments. This means setting key targets and KPIs on the most material topics, and publicly reporting progress on these indicators. Another leverage of activation is the implementation of lighthouse programs to drive stakeholder collaboration and impact.

If you are looking to get prepared for the updated standards or are preparing a new materiality assessment, get in touch with Johana Schlotter at johana@finchandbeak.com or call +31 6 28 02 18 80 to hear about how Finch & Beak can support you in meeting your ambitions.

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.